Life insurance is an essential component of financial planning, providing a safety net for your loved ones in times of need. Two of the most popular options in the realm of life insurance are Term Life Insurance and Whole Life Insurance. While both serve the purpose of offering protection, they differ significantly in their structure, benefits, and suitability for various financial goals. In this article, we will explore the unique differences between Term Life Insurance and Whole Life Insurance to help you make an informed decision.

Term Life Insurance: Protection for a Defined Period

Term Life Insurance is like renting protection for a set period, typically ranging from 10 to 30 years. Here’s what sets it apart:

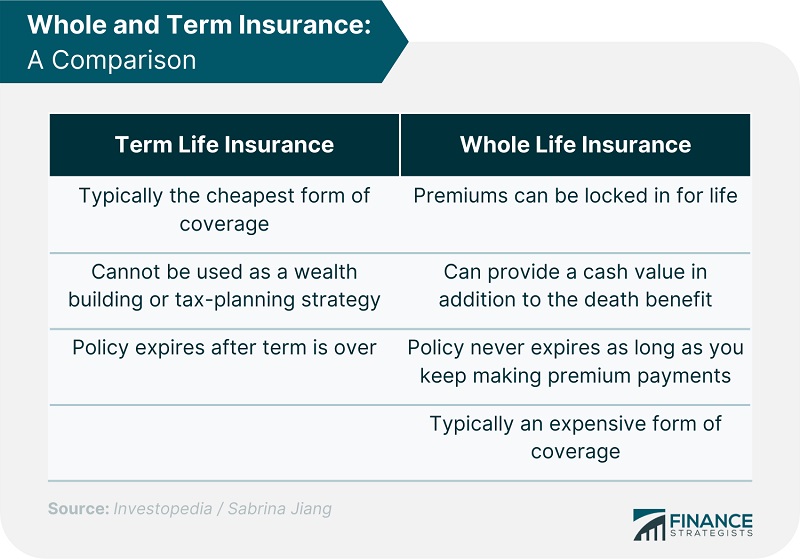

- Duration: Term Life Insurance provides coverage for a specific term. If the policyholder passes away during the term, the beneficiaries receive a tax-free death benefit. However, if the term expires before a claim is made, there is no payout.

- Affordability: Term policies are generally more affordable than whole life policies. They are a cost-effective way to secure a significant death benefit for your family while maintaining a tight budget.

- Customization: Term policies are highly customizable. You can choose the term length that aligns with your financial responsibilities, such as until your children graduate or your mortgage is paid off.

- No Cash Value: Term Life Insurance does not build cash value or savings. It’s pure insurance, designed to provide financial support to your loved ones if you pass away during the term.

- Renewability: Some term policies offer the option to renew at the end of the term, but the premiums typically increase significantly as you age.

Whole Life Insurance: Lifelong Protection with Cash Value

Whole Life Insurance is a permanent life insurance policy designed to provide lifelong coverage. Here’s what makes it unique:

- Lifelong Coverage: Whole Life Insurance offers coverage for your entire life. As long as you pay the premiums, your beneficiaries are guaranteed a death benefit whenever you pass away.

- Cash Value: A significant differentiator is the cash value component. A portion of your premiums is invested by the insurance company, and this cash value grows tax-deferred over time. You can borrow against or withdraw this cash value for various financial needs.

- Level Premiums: Premiums for Whole Life Insurance policies are generally level and remain the same throughout your life. This predictability can be helpful for long-term financial planning.

- Tax Advantages: The cash value growth is tax-deferred, and in many cases, the death benefit is paid out to beneficiaries tax-free. This makes Whole Life Insurance an attractive estate planning tool.

- Asset Protection: The cash value of a Whole Life Insurance policy is often protected from creditors in many states, providing an additional layer of financial security.

- Dividends: Some Whole Life Insurance policies, known as participating policies, may pay dividends to policyholders. These dividends can be used to reduce premiums, purchase additional coverage, or accumulate as cash value.

Choosing Between Term and Whole Life Insurance

The choice between Term Life Insurance and Whole Life Insurance depends on your financial goals and circumstances:

- Choose Term Life Insurance if: You want affordable, temporary protection to cover specific financial responsibilities, like a mortgage or your children’s education. You value flexibility and are comfortable with not building cash value.

- Choose Whole Life Insurance if: You seek lifelong coverage, cash value growth, and tax benefits. Whole Life Insurance is suitable for estate planning, wealth accumulation, and leaving a legacy.

In Conclusion

Term Life Insurance and Whole Life Insurance serve different purposes in the realm of life insurance. Your choice should align with your financial goals, budget, and the level of financial protection you want to provide for your loved ones. Understanding the unique differences between these two insurance options is essential for making an informed decision that best suits your needs.